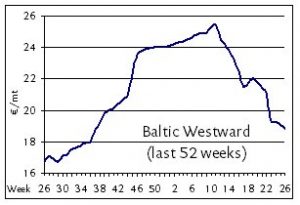

[27 JUNE 2018] With both European holidays and sluggish summer industrial trends setting in, pressure continues to grow on rates in the northern short sea markets even as owners manage to keep discounts limited. Operating costs, as always the basement level for rates to fall, have themselves taken a hit in recent weeks with bunker prices having progressively fallen, giving owners one fewer negotiating tool in keeping rates steady, if not higher. Freights in the high teens of EUR 17-18/mt on the Baltic westward routes from Balticum to ARAG (based on 3,000mt general cargo parcels) have moved slowly but surely into the mid teens of EUR 15-16/mt on the same run, brokers report. ECUK cargoes of 5,000mt are still securing around EUR 10-12/mt, depending on terms, to ARAG. Southbound spot freights remain relatively more attractive as southern European trade regions continue to attract higher activity and firmer rates than their northern counterparts. Agri-prods with stowage of 44-48′ are seen fetching EUR 24-26/mt, traders report, on business from the Upper Baltic to the French Mediterranean, more or less unchanged from rates on the same run since late May. Similar rates are reported as concluded on WCUK/Marmara business. Northbound rates from the Spanish Med to ARAG are fetching high teens of EUR 16-18/mt on mid-size parcels of 5,000mt while the same to the Upper Baltic is getting as high as EUR 22/mt. Upper Baltic to Ireland is still in the lower EUR 20s/mt, we are told, with owners keeping charterers at bay with EUR 21/mt as the lowest offer accepted.

[27 JUNE 2018] With both European holidays and sluggish summer industrial trends setting in, pressure continues to grow on rates in the northern short sea markets even as owners manage to keep discounts limited. Operating costs, as always the basement level for rates to fall, have themselves taken a hit in recent weeks with bunker prices having progressively fallen, giving owners one fewer negotiating tool in keeping rates steady, if not higher. Freights in the high teens of EUR 17-18/mt on the Baltic westward routes from Balticum to ARAG (based on 3,000mt general cargo parcels) have moved slowly but surely into the mid teens of EUR 15-16/mt on the same run, brokers report. ECUK cargoes of 5,000mt are still securing around EUR 10-12/mt, depending on terms, to ARAG. Southbound spot freights remain relatively more attractive as southern European trade regions continue to attract higher activity and firmer rates than their northern counterparts. Agri-prods with stowage of 44-48′ are seen fetching EUR 24-26/mt, traders report, on business from the Upper Baltic to the French Mediterranean, more or less unchanged from rates on the same run since late May. Similar rates are reported as concluded on WCUK/Marmara business. Northbound rates from the Spanish Med to ARAG are fetching high teens of EUR 16-18/mt on mid-size parcels of 5,000mt while the same to the Upper Baltic is getting as high as EUR 22/mt. Upper Baltic to Ireland is still in the lower EUR 20s/mt, we are told, with owners keeping charterers at bay with EUR 21/mt as the lowest offer accepted.

Get weekly updates from all the European short sea markets by subscribing to the BMTI SHORT SEA REPORT today.