NASDAQ-listed owner-operator Pangaea Logistics Solutions [PANL] says it plans to offer shareholders a quarterly dividend for the first time since going public in 2014. The US bulk carrier firm says it will pay US$ 0.035 from 11 June. CEO Ed Coll said the company had a proven business model and that after reinvesting profits in operations, Pangaea expected to become a leading “growth and income” company that cares about enhancing shareholder value. The company says it has managed to stay profitable, despite the ongoing dry bulk crisis, by offering logistical solutions to industrial clients with its owned and chartered-in fleet. Pangaea boasted income of US$ 3.7m against revenues of US$ 79.5m in Q1-2019.

Greek owners are said to be little nervous about 2020 with the upcoming challenge to meet the now sulphur cap standards. Some believe this could lead to a three or four-tier market. The uncertainty is worrying them without doing too much about it. The Atlantic chartering market is lacking momentum, whilst South Africa is flourishing and of course the South American area is still being dominated by Kamsarmax demand, whilst other sizes are trailing. Off the Continent, voyage rates for local trading are equivalent to US$ 9,000 daily for Ultramax vessels. Scrap charterers were seeing US$ 15-16,000 daily for a trip to Bangladesh which sounds unrealistic. Handysize freight rates have been about holding with a 32,000 dwt fixed into the central Med in the region of US$ 9,500 daily with delivery in the Baltic. The dearth of inquiry from Med-Black Sea is keeping rates at pretty low levels. On the other hand, achieving the equivalent of US$ 11,000 daily on a 62,000 dwt from West to East Med is not to be sniffed at.

Having had a relatively beneficial week, Capesizes start to flatten as the week ends with owners hoping that sentiment stays in their corner with trends moving sideways and some already trending downward. Front haul trips seem to have already peaked with the mid US$ 20,000s moving back into the US$ 24,000s and Pacific RVs into the US$ 11,000s. With Vale’s output very much in question and US-China trade conflicts at the fore, it remains to be seen what May has to give for this most volatile of bulk carrier sectors. But owners remain optimistic as ever. Panamaxes continue to enjoy their day in the sun with solid improvements on all freights observed across the board and charterers reluctantly giving premiums over last-done levels on nearly every rate. Front hauls that were getting low US$ 17,000s early in the week are now commanding high US$ 17,000s and even as much as US$ 18,000 daily in some cases. With little reason to do otherwise, Supramax owners are pushing for generously improved rates on all freights coming from the USG as more than US$ 12,000 daily has been observed on freights to the Continent and US$ 18,000 on front hauls with NoPac redelivery. The rest of the market is less buoyant by comparison, but owners are undoubtedly inspired to seek higher freights on nearly every rate.

To read shipbroking analysis like this every day, subscribe to the BMTI Daily Report.

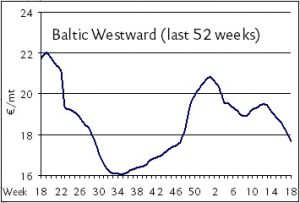

Declines in freights seem to have started to accelerate as the days of May lengthen with the lingering impact of holiday-strewn weeks having the expected braking effect on business activity in general. Charterers have given up trying to play nice for the time being as owners note a more aggressive attempt to push freights to new lows. Cargo demand, despite being promised to return in earnest after Q1, remains less than spectacular, to put it nicely. Even for a European coaster market that has seen very little tonnage expansion in recent years, and one that remains thankfully tightly-bound to cargo demand, the wide availability of tonnage is undeniable. High teens that were tracked for most of the year on the westward Baltic route—from Balticum to ARAG—in the range of EUR 18-20/mt are now moving toward EUR 16-17/mt and lower, brokers report. Longer runs from the German Baltic to WCUK are looking at mid-low EUR 20s/mt of about EUR 23-25/mt, depending on terms. This remains true, although traders are already assuming the same business will be going for EUR 22-23/mt by the end of the month. The reverse trip from WCUK to the lower Baltic is seeing 3,000mt general cargoes fix middle teens of EUR 14-15/mt.

Declines in freights seem to have started to accelerate as the days of May lengthen with the lingering impact of holiday-strewn weeks having the expected braking effect on business activity in general. Charterers have given up trying to play nice for the time being as owners note a more aggressive attempt to push freights to new lows. Cargo demand, despite being promised to return in earnest after Q1, remains less than spectacular, to put it nicely. Even for a European coaster market that has seen very little tonnage expansion in recent years, and one that remains thankfully tightly-bound to cargo demand, the wide availability of tonnage is undeniable. High teens that were tracked for most of the year on the westward Baltic route—from Balticum to ARAG—in the range of EUR 18-20/mt are now moving toward EUR 16-17/mt and lower, brokers report. Longer runs from the German Baltic to WCUK are looking at mid-low EUR 20s/mt of about EUR 23-25/mt, depending on terms. This remains true, although traders are already assuming the same business will be going for EUR 22-23/mt by the end of the month. The reverse trip from WCUK to the lower Baltic is seeing 3,000mt general cargoes fix middle teens of EUR 14-15/mt.

The decent handful of new TCs that came through for the Capesizes at midweek were not repeated by the end of the week, but no bother. Sentiment has been sufficiently triggered to start rising once again as the long-delayed requirements of the holiday period seem to be again entering the spot market with employment enquiries being reported by owners in the Atlantic and Pacific alike. Front hauls have been broadly upgraded with as much as US$ 23,500 daily on offer for standard tonnage from the Continent into the CJK area. Voyage rates enjoy another boost as well with Brazil/China climbing back over the US$ 15/mt marker with some owners already claiming to have US$ 16/mt on lock for end-May.

Perhaps inspired by the same gust of wind that has lifted the Capes—not to mention a new sense of purpose in the East—Panamax freights are firming a little bit faster, suggesting potential for a real recovery by next week, assuming trends hold steady. Front hauls have been getting fixed in the mid US$ 17,000s we are told, though this run is still too little frequented to make a fair assessment. Aussie rounds are pushing toward US$ 10,000 on Kamsarmaxes.

Improvements build for Supramaxes on Black Sea delivery with front hauls said to be hovering under US$ 13,000 daily on modern ships. Trans-Atlantic trades ex-USG remain problematic, but minerals on Tess 58s are securing steady rates of US$ 11,000 and up on UKC-Med redelivery with talk of US$ 11,500 on the horizon for the same business. Indo rounds are onwards and upwards with Supramax tonnage having set the new high water mark at US$ 9,500.

To read shipbroking analysis like this every day, subscribe to the BMTI Daily Report.

Impairments on credit for shipping and petroleum investments of Danske Bank fell in the first quarter of the year, according to the Danish bank’s newest interim report. Loan impairment charges saw a “significant reduction” in the quarter against loan exposures to the industries of shipping, oil and gas, said the report, noting that high reversals were especially seen in the area of Norwegian shipping, oil and gas. Net reversals of DKK 48m in total in the quarter were described as a “very low level” of impairment charges for the bank, according to the report, though these industries remain a “focus area” considering that the shipping market has had a “slower pickup” than was expected. Danske Bank’s Stage 1 gross exposure to shipping, oil and gas was at DKK 41.6m in the quarter, down from DKK 43.9m in Q4-2018.

Recent rainfall in Western Europe has boosted output forecasts for the EU wheat crop, though analysts warn that more rain will be required to avoid potential crop damage from drought. Forecasters remain positive for EU wheat as increased sowings and more favourable weather conditions this year (including a mild winter) suggest that output could return to normal after last year’s drought-afflicted harvest. The official forecast for EU common wheat production in the 2019-20 season was raised to 141.3 Mt this week, putting it a full 10% above last year’s output.

Capesize freights rose by as much as 38% last week, according to some metrics, with the recover in sentiment buoyed by the reopening of Vale’s Brucutu iron ore mine in Brazil and very strong voyage activity in the Pacific. With over 80% of bulk carrier trade said to be linked to iron ore (also, according to some metrics), the oversized influence of this commodity on the bulker trades can scarcely be underestimated. Rates have continued to climb as business resumed this week after the weekend, usually a sign of a bullish market, with TARV rates moving into the US$ 9,000s and Pacific round voyages climbing into the low teens of US$ 10-11,000 daily. Front hauls have already been fixing low US$ 20,000s of up to US$ 22,000 daily, according to some brokers’ reports, with shipowners having regained the control in negotiations for the first time in many weeks. These higher levels are nonetheless precarious, traders warn, as sentiment-driven as the Cape market is, another snap in geopolitical events could send rates tumbling as fast as they climbed in the final week of April. Owners hope that market fundamentals will solidify (as open tonnage tightens up) to keep this from happening.

After Easter break, one can’t but conclude that still not much is going on. The market in general remains pretty disappointing without any immediate ray of hope. Even though some brokers report a flurry of activity, others keep talking of a market trudging along. Indeed, the numbers talked and reported indeed suggest the latter. Off the Continent, Ultramaxes are being fixed in the low US$ 8,000s for a short local employment. The owners of a 56,000 dwt vessel have been seeing US$ 9,000 daily from scrap charterers for a trip to the East Med. Handy rates have been equally disenchanting with a 38,000 dwt booked for a Baltic round voyage with delivery Rotterdam at a rate of US$ 6,500 daily. The Black Sea remains a “graveyard” for the owners. Ultra-Supramax owners prefer to ballast away instead of taking front hauls of US$ 11-12,000 daily.

Adriatic Sea market: Traffic has been sporadic at best. Ammonium nitrate of 1,000mt has secured US$ 39-40/mt from Alexandria to Sarande (Albania). Steels of 1-2,000mt have fixed high US$ 30s/mt of up to US$ 37-38/mt ex-Nemrut to Split, brokers say. Standard grains of 5,000mt (46′) are being done from Yeisk into the Italian Adriatic at US$ 35/mt.

Turkish Med: As usual, import shipments to the Turkish Med have been considerable and trade has been steady in Q2 thus far. Fertilizers (urea) of 5-6,000mt have been routinely securing upwards of US$ 15/mt into Antalya from Damietta (and elsewhere in Egypt). Grains of 5,000mt (46′) ex-Novorossiysk to Mersin are being fixed at US$ 23-24/mt. Steels (2,000mt) from Iskenderun to Constanta have been reportedly concluded at about US$ 26-27/mt.

Operator Western Bulk Chartering announced that it has secured new debt financing and intends to raise US$ 15m in equity, ensured by its two main shareholders, in order to “support further growth” and strengthen its financial platform, said CEO Jens Ismar. The bond of US$ 35.1m (and US$ 31.74 outstanding) will be repaid in full, according to a statement from the company. WBC made an after-tax profit of US$ 4.2m last year, but suffered a big write-off in the second half of the year (US$ 10m) due to ill-timed time charter contracts signed by its Chile office. This year so far has also proven rather challenging for dry bulk markets, necessitating fresh financial support before the expected market recovery in the second half of 2019 in which the firm will “utilize the current market volatility” to its advantage, Ismar says.

Intended to provide so-called alternative financing for new shipping projects, General Credit Corp has been in development by Peter Georgiopoulos. The shipping magnate is reportedly working with at least two other executives in the publicly-listed shipping sphere, believed to be ex-Gener8 CFO Leo Vrondissis and ex-Gener8 VP of Finance George Fikaris. The fund is being developed in the growing realm of alternative finance, lending to shipowners (at higher margins) who can’t access funding from traditional ship lenders. Traditional maritime funding has become increasingly tight after the financial crisis and the collapse of generous shipping credit pre-2008. It remains unclear when the fund will be launched.

German bank NordLB, which recently announced its intention to completely withdraw from shipping, reported this week that it had sold off one portfolio of non-performing loans (NPLs) in shipping (nicknamed “Big Ben”) for a total of EUR 2.6 billion to US hedge fund Cerberus Capital Management. The portfolio, holding loans for 263 vessels, is categorized as 90% non-performing and will lower the bank’s total NPL shipping loans to EUR 4.9 billion from a previous level of EUR 7.5 billion at the end of last year.

For more of BMTI’s daily shipping analysis, subscribe to the BMTI DAILY REPORT today.

Again averting disaster at the last minute, Capesize freights pull back from oblivion to post even better upgrades than the start of the week, thanks to a return in chartering interest, moving trans-Atlantic RV rates well into the US$ 5,000s and front hauls to within range of US$ 19,000 daily. Actual time charter fixtures are still forthcoming, one hopes, but the fact that freight improvements are building steam rather than losing it suggests that this undervalued market is overdue some upward corrections. Pacific RVs hover in the US$ 4,000s, so they would have a ways to go to regain profitability, but given current trends, that remains plausible before month’s end. Now the Panamaxes find themselves a bit worse for wear than they were just a week ago with daily losses starting to pick up heft and charterers developing an allergy to getting involved in a market that seems to be swinging back into their favour. Activity has been sparse this week thus far and Atlantic business has slowed to a trickle on ECSA delivery with only a handful of rounds from the Pacific and back fetching around US$ 11,000 daily DOP on modern tonnage. Hanging on for dear life, Supramax owners are resisting a downturn in sentiment that is appearing to be increasingly inevitable as cargoes stay stubbornly slow. Period chartering is seen in stops and starts with short period deals on Tess 58s having done US$ 11,500 on Far East delivery with worldwide redel. NoPac RVs manage to stay in the high US$ 7,000s, but limited interest on Singapore-Japan redel could spell a sharper downturn as the week goes on. Black Sea front hauls are flat in the US$ 12,000s.

The world’s second-largest non-Chinese aluminium producer, Rusal, began new production operations last week at its Boguchansk aluminium smelter in Siberia. This added output essentially doubles the plant’s capacity to 298,000mt tonnes; the company is even considering adding more capacity, already, according to CEO Evgenii Nikitin. Rusal has been busy resuming output and shipments since the end of last year when sanctions imposed by the United States were lifted after nine months of negotiations that ended in founder Oleg Deripaska giving up his control of the company. While the company lost contracts in the sanctions period, it says it is busy winning supply contracts back for 2020 and expects to “restore lost positions” in its traditional markets, particularly in Asia and America. Shipments in Europe seem to have been less disturbed, but the new output activity and lifting of sanctions are likely to see increased aluminium shipments along European waterways as well. Rusal is also busy building a new smelter in Taishet set to launch late next year. The company expects worldwide aluminium demand to grow 3.7% this year to 68 Mt and keep growing at the same rate in 2020.

Rate recovery is still elusive for the nonperforming Capesize sector. A severe lack of demand having its way with spot freights. All things considered, they could be plummeting more sharply than they are given the wide range of tonnage currently available to charterers. But it would seem that more owners are just refusing to go any farther below breakeven, which has long since been passed. In fact, it’s hard to imagine a Capesize owner having secured any profit so far this year, such is the miserable base level for earnings at the moment. Pacific-based voyages have nonetheless stabilized for the most part with Brazil/China voyages holding firm in the range of US$ 11.6-11.7/mt. That kind of stability counts for something, and shouldn’t be underestimated, owners are advised to remind themselves. Everything is coming up Panamaxes, one could say, with only a shiver of trouble appearing in the eastern basin as Pacific round voyages seem to have peaked at US$ 8,000 daily. Indeed, most new RVs for next week are said to be trading in the high US$ 7,000s. This uggests that owners may once again find themselves struggling to keep rates in place. Atlantic Panamax owners, on the other hand, remain well-placed for the ongoing South American surge as tighter avails mean TARVs can move into the middle US$ 8,000s. Trouble in paradise for the eastern Supramaxes as charterers put on the brakes before the weekend. Rate gains have come to a halt in the eastern basin. Pacific RVs are still hovering at around US$ 9,000 for 58,000 dwt tonnage, but we do hear that charterers have been moving their ideas downward for early April positions. Western trends remain on the bullish side, at any rate, as USG delivery is still giving owners good reason to pursue higher-than-last rate levels. Front hauls ex-USG are still rising, albeit more slowly, with US$ 19,000s reported by some for CJK redel even as US$ 18,000s are the new standard area for eastbound Ultramaxes.

For more of BMTI’s daily shipping analysis, subscribe to the BMTI DAILY REPORT today.

Off like a light, the Capesize rebound of last week seems to have hit a wall at the start of this week with a very strong reversal of negative US$ 800-900 (or thereabouts) on the trans-Pacific RV taking those rates back into the low US$ 7,000s daily range. Few new fixtures have emerged so far this week, though that could still change by midweek, owners say. On the other hand, if the activity that helped buoy the spot markets last week doesn’t reappear quickly, there is a very good possibility that new downward corrections will start coming fast and furious. Voyage rates have remained stable so far with Brazil/ China unchanged in the area of US$ 11.9-12.0/mt. There does seem to be plenty of energy left in the Panamax markets with the positive momentum of last week pushing into this week and keeping trends bullish. TARVs look to be the most improved even as US$ 5-6,000s rates are still poor for any owners hoping to make a profit in this challenging market. Slightly more promising are front hauls, which are benefitting from a modest renaissance from South America as DOP rates ex-Brazil (open UKC-Med) are granting Kamsarmax ships upwards of US$ 16,000. Apart from the collapsing Black Sea front hauls (in a replay of the same on USG front hauls two weeks ago), Handy bulk rates remain rather steady in the Atlantic and even bullish on South America delivery. ECSA export trips are currently keeping the entire western market aloft, it would seem, with front hauls getting upwards of US$ 13,000 daily DOP to the Far East on tonnage of 58,000 dwt and even US$ 14,000 daily on Ultramax vessels exceeding 62,000 dwt. The USG/UKC trans-Atlantic trips are holding steady in the US$ 10-11,000 range on Tess 58s.

For more of BMTI’s daily shipping analysis, subscribe to the BMTI DAILY REPORT today.

Scorpio Bulkers [SALT] sold seven ships to China Merchant Bank Financial Leasing in a sale-and-leaseback deal wherein the owner will lease the ships back from the partially state-owned bank. Scorpio says it will add US$ 60m in liquidity from the deal.

The New York-listed dry bulk company, Eagle Bulk [EGLE], was pleased to announce in its new annual report to having secured a profit in 2018, offsetting a deficit in the year before. Last year saw revenue rise by 31% thanks to gains in the dry bulk market as a whole and a rise in available ship days for its vessels (the company purchased 12 Ultramax carriers in the last two years). Company CEO Gary Vogel says Eagle Bulk plans to continue executing its fleet renewal plan. A refinancing plan in 2018 also gave the company some US$ 65m in new liquidity, which helped it lower debt costs and extended maturation dates for existing loans. Revenue grew US$ 73.3m to US$ 310.1m in 2018, contributing to a new profit of US$ 12.6m in the year versus a deficit of US$ 43.8m the year before. For the first quarter of 2019, the company has already secured 90% of its ship days for its fleet at an average TCE of US$ 9,124 daily. Ahead of the 2020 sulphur regulations, Eagle Bulk says it will already have 37 of its ships fitted with scrubbers. The company fleet currently consists of 47 dry bulk carriers made up of Supramax and Ultramax ships.

Investment opportunities have thinned out for the bulk carriers in the year so far with freight rates under pressure, but near term prospects are still well-balanced between cargo and tonnage, according to Court Smith of VesselsValue at the recent German Ship Finance Forum in Hamburg. There is, however, a negative mismatch between expected tonne-mile growth and tonnage growth for nearly every bulker size, with the exception of one, Smith said. In terms of tonne-mile growth vs. supply growth in 2019, Smith expected to see -0.9% for Capesizes, -0.7% for Panamaxes, -0.9% for Supramaxes but + 0.4% for Handysize vessels. Given the overall “positive balance” in the Handysize sector, Smith recommends the smallest bulker size class as the best “top level” investment perspective for the current market.

For more of BMTI’s daily shipping analysis, subscribe to the BMTI DAILY REPORT today.

Charterer interest in Panamaxes fades

Enquiry for Panamaxes has apparently dried up in the way that Cape interest dried up in late February. (p. 1)

Long haul business stays active on Ultramaxes

From WCCA, Ultramax tonnage was shown US$ 8,000 for a trip to the Med-Continent area. (p. 2)

Containership rates continue steady decline

The modest but steady downward trend in container freights remained well in place last week with an average of 4-5% lost on freights (down 4.6% on the SCFI), showing not a single positive progression in any single rate, unlike weeks past. (p. 2)

For more of BMTI’s daily shipping analysis, subscribe to the BMTI DAILY REPORT today.

An upsurge in activity across the eastern basin has done wonders for the long-beleaguered Supramax markets with average rates for rounds up by at least US$ 500 week-on-week and, in some cases, nearly US$ 1,000 higher than a week ago. Standard rounds are trading in the US$ 6-7,000s daily on tonnage of 58,000 dwt. Indonesia rounds have been especially improved with a massive US$ 2,000 week-on-week improvement in average rates from South China to ECI, climbing into the US$ 6,000s by week’s end. Handysize markets have been comparatively more subdued than their high-flying Supramax brethren, although eastern trends have been favourable to the smaller sized segment as well. Pacific rounds via Singapore-Japan from CJK edged up into the US$ 4,000s after spending the past week in the high US$ 3,000s. Southeast Asia has been especially buoyant with tonnage of 28,000 dwt getting over US$ 6,000 daily with sugar from Thailand to Indonesia (though standard cargoes are more likely to fetch US$ 5,000s on this run). Tonnage of 38,000 dwt is securing high US$ 5,000s daily on NoPac trips to South Korea.

For more of BMTI’s daily shipping analysis, subscribe to the BMTI DAILY REPORT today.

Slowly, it would seem that the Capesize freights are stabilizing, with the possible exception of long hauls on TARV and front haul terms, with voyages nearly all trending flat or slightly higher. Aussie voyages appear to be the most buoyant at the moment with upwards of US$ 5.3/mt being reportedly negotiated on tonnage of 170,000mt from West Australia to South China. This is around US$ 0.3-0.5/mt higher than the rate was trading at this time last week. There has been some considerable slowing in coking coal traffic from Australia to China, traders report, with customs delays causing vessels to have waiting times of up to 60 days to unload at Chinese ports. This, combined with recently disrupted operations at two coal mines in Australia, is expected to put a brake on Australian coal exports for the near term.

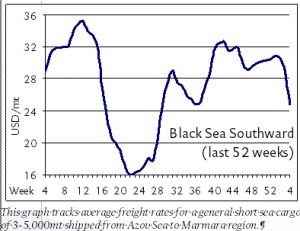

Freights continue to fall rather precipitously in the Azov trades with owners continuously coming up short on the cargo side of the market. Owners say rates have fallen so quickly since their recent peak at the end of 2018 that they are down as much as US$ 9/mt now from that point, roughly a third, considering that Azov/Marmara rates are currently in the low US$ 20s/mt on grain of 5,000mt (46′). A veritable perfect storm of bearish conditions—extended port delays at Russian ports, the stronger rouble, increased domestic commodity demand (along with lower international demand), rising domestic prices and the fairly mild winter—are conspiring to make this winter a tougher than usual one for shipowners. Kherson/TBS has stabilized at US$ 20-22/mt.

Freights continue to fall rather precipitously in the Azov trades with owners continuously coming up short on the cargo side of the market. Owners say rates have fallen so quickly since their recent peak at the end of 2018 that they are down as much as US$ 9/mt now from that point, roughly a third, considering that Azov/Marmara rates are currently in the low US$ 20s/mt on grain of 5,000mt (46′). A veritable perfect storm of bearish conditions—extended port delays at Russian ports, the stronger rouble, increased domestic commodity demand (along with lower international demand), rising domestic prices and the fairly mild winter—are conspiring to make this winter a tougher than usual one for shipowners. Kherson/TBS has stabilized at US$ 20-22/mt.

Need more short sea news? Consider a subscription to the BMTI SHORT SEA REPORT.

Apart from a few late-reported fixtures that emerged at the end of the week, little if any guidance is visible for the sliding freight market for Capesizes. Front haul trips have assumed the mantle of most bearish route at the moment with losses of some US$ 1,000 between Thursday and Friday taking the assessment under US$ 27,000 daily. It is difficult to measure rate levels with so few fixtures available, but suffice it to say that charterers are having a good 2019 so far.

The periodic return of Panamax activity, assisted by more Continental demand than in weeks past, still fails to shift the freight trend from its downward path. Shipowners are hoping against hope that the market’s overhang of available tonnage will finally be arrested, but as long as cargo demand can be held back, there is little likelihood of the same in the near term. Period chartering remains one highlight with upwards of US$ 10,750 daily rumoured as fixed for 5-8 months on a Kamsarmax with worldwide redel.

Atlantic delivery remains fraught for Handy bulk owners, though talk of high US$ 13,000s fixed from the Baltic to AG on Supramaxes has been encouraging for owners. Most new activity remains isolated within the eastern basin where Pacific round voyages have stabilized in the US$ 7,000s daily area, leaving most of the losses to the West. Indonesia rounds on Vietnam redelivery are said to have fixed APS terms at about US$ 7,000 daily on tonnage of 58,000 dwt.

For more of BMTI’s daily shipping analysis, subscribe to the BMTI DAILY REPORT today.

The last few weeks of 2018 were among the best of the entire year itself for northern European short sea owners as a long-delayed recovery in freight levels finally transpired and put owners in the position of power that they had been denied for most of the preceding eleven months. Trading volumes fell significantly over the holidays with nearly all market participants away from their desks and momentum taking freights over the transom of the no man’s land between years. With real trading resuming in earnest this week, the first full business week of the year, owners are hoping that any pressure that developed over the holidays will again be relieved as market fundamentals take over once again. Colder weather conditions will surely play a part with wind and ice-related delays slowing turnaround times and shortening general availabilities. At any rate, southbound traffic from WCUK into the Italian Adriatic has been holding steady with freights still in the low EUR 30s/mt on general parcels of 3-5,000mt. Northbound rates from the West Med to ARAG are fetching upwards of EUR 19/mt, but more likely to be in the EUR 17-18/mt unless charterers express some degree of urgency. There is a tangible sense of renewed optimism among owners in the North Sea and Baltic Sea trades that momentum will remain on their side, at least in these early days, though they are still in desperate need of evidence of the same before it starts to look like premature hope. The westward trades from the upper Baltic into the ARAG area are fixing low EUR 20s/mt of up to EUR 21-22/mt, which is quite an improvement on the mid-high teens of EUR 16-18/mt observed just a few weeks before. Rates from the German Baltic to Ireland have been recorded up to EUR 28.5/mt on generals of 3,000mt, but at least one broker claims the average rate on this business is more likely in the area of EUR 26.5-27.5/mt. All things being equal and based on the persistently stagnant fleet growth of the European market, any uptick in demand will most likely be immediately felt in rate levels. Owners are praying that such an uptick arrives as soon as possible.

Some of the shine is already off of the Capesizes as the week comes to an end with the reality setting in that charterers are far from anxious to fix any major business this early in the year. As such, corrections come nearly immediately on the high-flying Pacific RVs, neutralizing the gains they made yesterday by an equal US$ 400-500 to bring them back to US$ 14,000. The rest of the market is moving more or less sideways, awaiting the first full business week.

Some of the shine is already off of the Capesizes as the week comes to an end with the reality setting in that charterers are far from anxious to fix any major business this early in the year. As such, corrections come nearly immediately on the high-flying Pacific RVs, neutralizing the gains they made yesterday by an equal US$ 400-500 to bring them back to US$ 14,000. The rest of the market is moving more or less sideways, awaiting the first full business week.

Encouragingly active at the tail end of the week than at the beginning, Panamax fixing has still failed to turn trends around from their bearish paths. Period business has been especially prominent in the first week of the year with several short period deals (3-5 to 4-6 and 4-8 months) being concluded in the US$ 11,000s on standard tonnage and up to US$ 13,500 daily and higher on modern Kamsarmax tonnage of 82,000 dwt. The spot markets are nonetheless tepid.

If fixtures were any indication, one would think the Handy bulk is on the rebound. And that may still be the case in another day or two, but so far they increase in chartering activity has failed to make a dent in the resolutely downward trend of USG Supramax rates, which have fallen to US$ 26,000 daily on the benchmark for front hauls to CJK. Eastern activity has helped keep rates in the eastern hemisphere far more stable, all things considered, with mineral demand via Southeast Asia already taking a lead role.

For more of BMTI’s daily shipping analysis, subscribe to the BMTI DAILY REPORT today.

Panamaxes cheaper than Ultramaxes on trips from ECSA

The ECSA has been steady with Ultramaxes fixed at US$ 15,250 daily plus US$ 525,000 BB whilst Panamaxes have been cheaper; hence chars are trying to change to Panamaxes whenever possible. (p. 1)

Eastern Handysize rates stay in the doldrums

Owners of 32,000 dwt tonnage were talking middle US$ 5,000 daily for a trip from China to USWC. (p. 1)

Scrap prices correcting as Turkish mills buy less

Spot market prices for scrap metal in Europe took a sharp fall last week in sync with falling steel prices and cooling demand to Turkish steel mills. (p. 2)

For more of BMTI’s daily shipping analysis, subscribe to the BMTI DAILY REPORT today.

Hong Kong bulk carrier firm, Pacific Basin, has concluded a US$ 40m loan facility with Danish Ship Finance, it announced last week. The facility, intended for seven years duration, is an extension of the company’s existing loan agreement with DSF and will be secured by the same 19 ships under the initial facility. Pacific Basin says that the new facility was achieved at a competitive interest rate and will go to improve the company’s financial flexibility.

Scorpio Bulkers and Tankers have upgraded their plans for extensive installation of scrubbers across their fleets with the stated intention of “practically all” of its owned and chartered Kamsarmax and Ultramax ships. Scorpio Bulkers fleet amounts to 56 owned and chartered vessels of which 19 are Kamsarmaxes and 37 are Ultramaxes. With initial plans for open-loop scrubbers, eventually to be upgraded up to closed-loop units, overall investment will add up to US$ 42.4m for Scorpio Bulkers (28 vessels) and US$ 79.6m for Scorpio Tankers (52 vessels).

Having found shipping as one of the last frontiers of digitalisation, Hamburg-based TecPier has launched as an investment organisation to discover start-ups to support with funding, operational resources and networking with established industrial partners in the maritime sector. The company plans to invest mainly in start-ups in the pre-seed and seed phases to guide young companies in their early development phase. TecPier has formed partnerships with Zeaborn Group, BitStone Capital and Inno Real with shareholders in VC and shipping. Founding partner, Johannes Winkler, says TecPier has found over 150 start-ups with real potential for investment and development in the arena of shipping digitalisation.

Secondhand bulkers remain very undervalued, says Martin Rowe, head of Clarksons Platou, given their earnings potential. The current price for a ten-year-old Capesize, said Rowe at a maritime conference in Hong Kong, is some 30-50% of what it should be.

For more of BMTI’s daily shipping analysis, subscribe to the BMTI DAILY REPORT today.

They had a good run, but looking at the declines that have hit the Capesizes at the end of the week, it would seem like classic over-correction being swiftly neutralized following a false dawn of spot market recovery. No route is spared with Pacific round voyages—appropriately, considering their oversized improvements—taking the worst of the decline, losing more than US$ 2,000 to settle in the high teens of US$ 17-18,000. Front haul trips, meanwhile, slip into the mid US$20,000s of about US$ 25,000 daily after fading from the high US$20,000s set at midweek. Voyages have also come under heat as West Aussie rates to China slide to just above US$ 8/mt and Brazil/China voyages fall under US$ 17.5/mt.

If not quite at a boiling point, Panamaxes continue enjoying positive sentiment pushing rates higher yet with TARVs now likely to trade at US$ 14,000 daily (or just below) on early December dates, much improved from the US$ 13,000s of last week and weeks before. Pacific RVs are also holding to just over US$ 9,000 daily on standard 72-76,000 dwt tonnage with a notable upside still very much in place. Front hauls stabilized at around US$ 20,000 daily with slight improvements still more likely than slight discounts. Rumours abound with a market still in flux: period rates, while not taking the market by storm, are still fixed on a regular basis. There is one small Panamaxes (rumoured to be 62,000 dwt) fixed at US$ 19,500 for medium period ex-Veracruz on worldwide redelivery. Nickel ore runs on similar sizes (64-66,000 dwt) from South China have been secured at US$ 8,250 daily via Indonesia and back.

Period chartering seems to be returning to some degree to the Handy bulk sector with US$ 8-9,000 rates being done on Tess 52 tonnage from Southeast Asia on worldwide redel (3-5 months of trading). The big story in the Atlantic remains the USG with US$ 26,000 the newest high water market set for front hauls on Tess 58 ships. In the East, inter-Pacific trips are also fetching middle-high US$ 8,000s with such rates seen on 52-56,000 dwt ships from NoPac booked for trips south to Vietnam or Thailand.

To see more of BMTI’s daily dry bulk analysis, subscribe to the BMTI DAILY REPORT today.

Capesize freights start the week in limbo

Starting the week on an undecided, Capesizes trend largely sideways with only the Pacific RVs taking any considerable damage, losing only US$ 200-300 to settle in the mid US$ 8,000s. (p. 1)

Promising signs for Handies via South Africa

South African brokers expect a rush for tonnage for first half December dates, which already has inspired owners of a 56,000 dwt open ECI to indicate her for a South African RV at US$ 13,000 daily. (p. 2)

Modest uptick in box rates on USEC redelivery

More influential was the Shanghai-to-USEC route, up 3.5% week-on-week to hit US$ 3,739/FEU while the corresponding USWC redel (20% of the SCFI) fell by 1.8% to trade at US$ 2,529/FEU. (p. 2)

To see more of BMTI’s daily dry bulk analysis, subscribe to the BMTI DAILY REPORT today.

In the US Gulf, owners are grappling with weakening demand with petcoke charterers rating a 56,000 dwt at US$ 16,000 daily versus owners’ rate of US$ 18,000 daily for a trip to East Med. Even Ultramax tonnage is rated below US$ 20,000 by petcoke charterers. A 28,000 dwt has been fixed from Rio Haina for a 15-day local employment at about US$ 12,000 daily. And owners of 1984-built, 42,000 dwt vessel must consider themselves lucky to have been given the opportunity to fix her from Atlantic Columbia to North Spain at around US$ 15,500 daily. From the ECSA, front haul rates for Ultramax tonnage are hovering at around US$ 15,500 daily plus US$ 550,000 BB. The midterm future for Handysize tonnage sounds promising. With a new crop coming on stream, coastal business has already been given a boost that brokers expect to be extended to trans-Atlantic business for which rates of around US$ 18-20,000 for 36-40,000 dwt tonnage sounds realistic.

The East has not been very generous with the owners, who are aghast at the numbers that they are seeing, which has already led a couple of owners to contemplate ballasting to the Atlantic, which for eco tonnage may be an option whereby bunkers costs are more bearable than for other less eco tonnage. The owners of a 58,000 dwt ship were proposed around US$ 6,750 daily for the first 44 days to be followed with US$ 10,250 daily for the balance up to six months. Handy charterers did not hesitate to propose US$ 7,000 daily on a 38,000 dwt for a trip from P.I. to the PG, which the owners turned down asking above US$ 10,000 daily. Coal charterers were rating other similar tonnage at US$ 9,500 daily for a trip from P.I. via Indonesia to China with coal.

To benefit from BMTI’s daily shipbroker analysis, subscribe to the BMTI DAILY REPORT today.

Bearish trends continue to bite in Handy market

Gravity has started to weigh heavier on Handy bulk at midweek with declines most notable on the long hauls into the Far East with ECSA delivery to North China losing some US$ 100-300 since Monday to settle at US$ 17,000 on modern Ultramaxes. (p. 1)

Hope remains in place for Panamax owners

Panamax shipbrokers are cautiously optimistic that market conditions will remain stable, hoping for an end-of-the-year spike. (p. 1)

Enduring dryness threatens European waterways

Continuing and historically high dry conditions across Europe have seen water levels drop such that key waterways have started to reroute traffic or stop it altogether. (p. 2)

To benefit from BMTI’s daily broker analysis, subscribe to the BMTI DAILY REPORT today.

Capesize voyages enjoy solid weekly gains

New voyages on 150,000mt from South Africa to ARAG, for instance, have climbed into the range of US$ 9.7/mt, which is around US$ 2/mt higher than only a week previous. (p. 1)

Continued stability in Black Sea Handy bulk

The Black Sea remains relatively stable with grain charterers seeing US$ 24-25/mt for 30,000mt ex-Novo to Dunkirk, whilst talking US$ 23/ mt. (p. 1)

Coasters: New optimism in Baltic-based trades

Rates between the German Baltic and ARAG have edged into the area of US$ 14/mt in both directions with talk that US$ 15/mt is already in talks for late next week on upper Baltic delivery. (p. 2)

To benefit from BMTI’s daily shipbroker analysis, subscribe to the BMTI DAILY REPORT today.