From the Desk of a Continental Broker: The solidity of the markets’ performance is unquestionable. Panamaxes are leading the way. Encouragingly, charterers continue to take tonnage from the East with a most recent peak of US$ 17,000 daily done from Mumbai area via ECSA to the East. Capers are less fortunate with rates declining. But talking in more general terms, sentiment remains unclouded. Off the Continent, scrap charterers were bidding a rate of US$ 14,500 daily for a 57,000 dwt on a trip to the East, which isn’t great, whilst ice-classed tonnage of 56-58,000 dwt vessel was being bid US$ 15,000 daily from Gibraltar via the Russian Baltic back to the Med, which is better. A Rouen/Algeria voyage for 30,000mt was rumoured as done at US$ 19/mt and equates to around US$ 10,500 daily including 450 miles of ballast to the loading port.

The Black Sea is short of Ultra-Supra vessels willing going east of Suez. But the rate structure is hardly affected with Supra tonnage worth around US$ 18-19,000 daily whilst Ultramaxes are worth around US$ 21-22,000 daily. The US Gulf is in a bit of a downward spiral. After a front haul trip on Ultramax tonnage was done at US$ 23,000 daily thence US$ 22,000 daily and US$ 20,500 daily respectively and now US$ 19,500 daily—which seems to have failed, however. A 58,000 dwt was booked at US$ 21,000 daily to WCSA, not good at all in comparison with earlier fixtures done. In line with it, Handies have also been dragged down with 32-34,000 dwt worth just about US$ 13-13,500 daily for a trip across the Atlantic or US$ 14,500 for the larger 36-38,000 dwt vessels, respectively Further, a trip to the West Coast pays around US$ 16-17,000 daily, depending on the vessel or whether charterers are jitterbugs.

In the ECSA, Ultramax tonnage has been in the limelight with Raffles surpassing everyone by booking an Ultra at US$ 15,750 daily plus US$ 575,000 BB to load sugar to the East. T/A rates for Supra tonnage are hovering at around US$ 17,500 daily whilst for front haul a rate of US$ 14,000 daily plus US$ 400,000 BB seems to have been agreed. In contrast, it has been very quiet on the Handy front. There appears to be no let up in the East where the owners of 28,000 dwt tonnage want US$ 10,500 for a trip from north China to India, or coal charterers rating a 37,000 dwt at US$ 10,000 daily for a quick 15-20 day employment ending Japan-Korea range.

The Red Sea has developed into the most intriguing market where every charterer risks to take a beating. Casillo has now increased its cargo size to 40-45,000mt, suiting an Ultramax-Supramax, but with the lack of tonnage in the area, the headaches to cover this cargo are unlikely to disappear soon.

Want more exclusive broker viewpoints like this? On a daily basis? Subscribe to the BMTI Daily Report today.

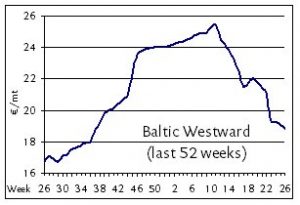

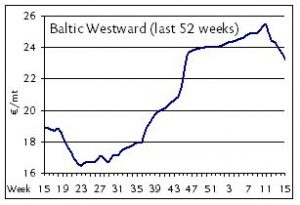

[27 JUNE 2018] With both European holidays and sluggish summer industrial trends setting in, pressure continues to grow on rates in the northern short sea markets even as owners manage to keep discounts limited. Operating costs, as always the basement level for rates to fall, have themselves taken a hit in recent weeks with bunker prices having progressively fallen, giving owners one fewer negotiating tool in keeping rates steady, if not higher. Freights in the high teens of EUR 17-18/mt on the Baltic westward routes from Balticum to ARAG (based on 3,000mt general cargo parcels) have moved slowly but surely into the mid teens of EUR 15-16/mt on the same run, brokers report. ECUK cargoes of 5,000mt are still securing around EUR 10-12/mt, depending on terms, to ARAG. Southbound spot freights remain relatively more attractive as southern European trade regions continue to attract higher activity and firmer rates than their northern counterparts. Agri-prods with stowage of 44-48′ are seen fetching EUR 24-26/mt, traders report, on business from the Upper Baltic to the French Mediterranean, more or less unchanged from rates on the same run since late May. Similar rates are reported as concluded on WCUK/Marmara business. Northbound rates from the Spanish Med to ARAG are fetching high teens of EUR 16-18/mt on mid-size parcels of 5,000mt while the same to the Upper Baltic is getting as high as EUR 22/mt. Upper Baltic to Ireland is still in the lower EUR 20s/mt, we are told, with owners keeping charterers at bay with EUR 21/mt as the lowest offer accepted.

[27 JUNE 2018] With both European holidays and sluggish summer industrial trends setting in, pressure continues to grow on rates in the northern short sea markets even as owners manage to keep discounts limited. Operating costs, as always the basement level for rates to fall, have themselves taken a hit in recent weeks with bunker prices having progressively fallen, giving owners one fewer negotiating tool in keeping rates steady, if not higher. Freights in the high teens of EUR 17-18/mt on the Baltic westward routes from Balticum to ARAG (based on 3,000mt general cargo parcels) have moved slowly but surely into the mid teens of EUR 15-16/mt on the same run, brokers report. ECUK cargoes of 5,000mt are still securing around EUR 10-12/mt, depending on terms, to ARAG. Southbound spot freights remain relatively more attractive as southern European trade regions continue to attract higher activity and firmer rates than their northern counterparts. Agri-prods with stowage of 44-48′ are seen fetching EUR 24-26/mt, traders report, on business from the Upper Baltic to the French Mediterranean, more or less unchanged from rates on the same run since late May. Similar rates are reported as concluded on WCUK/Marmara business. Northbound rates from the Spanish Med to ARAG are fetching high teens of EUR 16-18/mt on mid-size parcels of 5,000mt while the same to the Upper Baltic is getting as high as EUR 22/mt. Upper Baltic to Ireland is still in the lower EUR 20s/mt, we are told, with owners keeping charterers at bay with EUR 21/mt as the lowest offer accepted. The holiday hangover has lingered over the

The holiday hangover has lingered over the  Losses have been rather substantial in the eastern Handy bulk trades in the past week as the monthly switchover and widespread holidays gave charterers all the excuse they needed to get rates reduced toward their preferences. In the event, Supra NoPac rounds lost US$ 500 week-on-week to settle in the lower US$ 11,000s after trading high US$ 11,000s just a week earlier. Indonesia rounds, meanwhile, shed some US$ 300-500 over the week, putting the South China delivery and redelivery round in the high US$ 10,000s of about US$ 10,750 daily on tonnage of 58,000 dwt. Period chartering has been done, though intermittently, with short periods of six months getting US$ 13,000 daily on Handymax tonnage of 54-56,000 dwt from Southeast Asia.

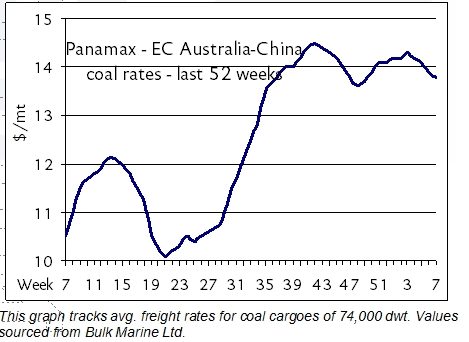

Losses have been rather substantial in the eastern Handy bulk trades in the past week as the monthly switchover and widespread holidays gave charterers all the excuse they needed to get rates reduced toward their preferences. In the event, Supra NoPac rounds lost US$ 500 week-on-week to settle in the lower US$ 11,000s after trading high US$ 11,000s just a week earlier. Indonesia rounds, meanwhile, shed some US$ 300-500 over the week, putting the South China delivery and redelivery round in the high US$ 10,000s of about US$ 10,750 daily on tonnage of 58,000 dwt. Period chartering has been done, though intermittently, with short periods of six months getting US$ 13,000 daily on Handymax tonnage of 54-56,000 dwt from Southeast Asia. The Panamax freight rates since last week are on the start to continue on their southbound trail but with low demand of grains from Chinese buyers.

The Panamax freight rates since last week are on the start to continue on their southbound trail but with low demand of grains from Chinese buyers.